The Pacific is warming, and early signals point to a potentially powerful Super El Niño in the making. If it develops as some models suggest, the effects on U.S. weather and energy markets could be significant, reshaping summer heat patterns, suppressing hurricane activity, and softening winter demand across key northern load zones. The result, taken together, could be a meaningful bearish shift in energy prices over the coming seasons.

Why El Niño Matters

El Niño is driven by warmer-than-normal sea surface temperatures in the equatorial Pacific, which alters atmospheric circulation and shifts the jet stream. That, in turn, changes how heat, precipitation, and storm activity are distributed across North America. Stronger events, sometimes described as "Super El Niños," tend to amplify those effects significantly, especially in winter. When sea surface temperature anomalies reach the thresholds that define a Super El Niño, the same mechanisms that characterize a moderate event become more intense and more persistent, with correspondingly larger market implications.

For markets, the main significance is that El Niño can reduce some of the most important weather-driven upside risks. It can limit the odds of prolonged, multi-region summer heat, suppress Atlantic hurricane activity, and tilt winter toward warmer conditions across the northern U.S. In each case, the result is some reduction in the likelihood of the extreme conditions that tend to tighten balances and drive price spikes. A Super El Niño raises the probability that these effects are not just present, but dominant.

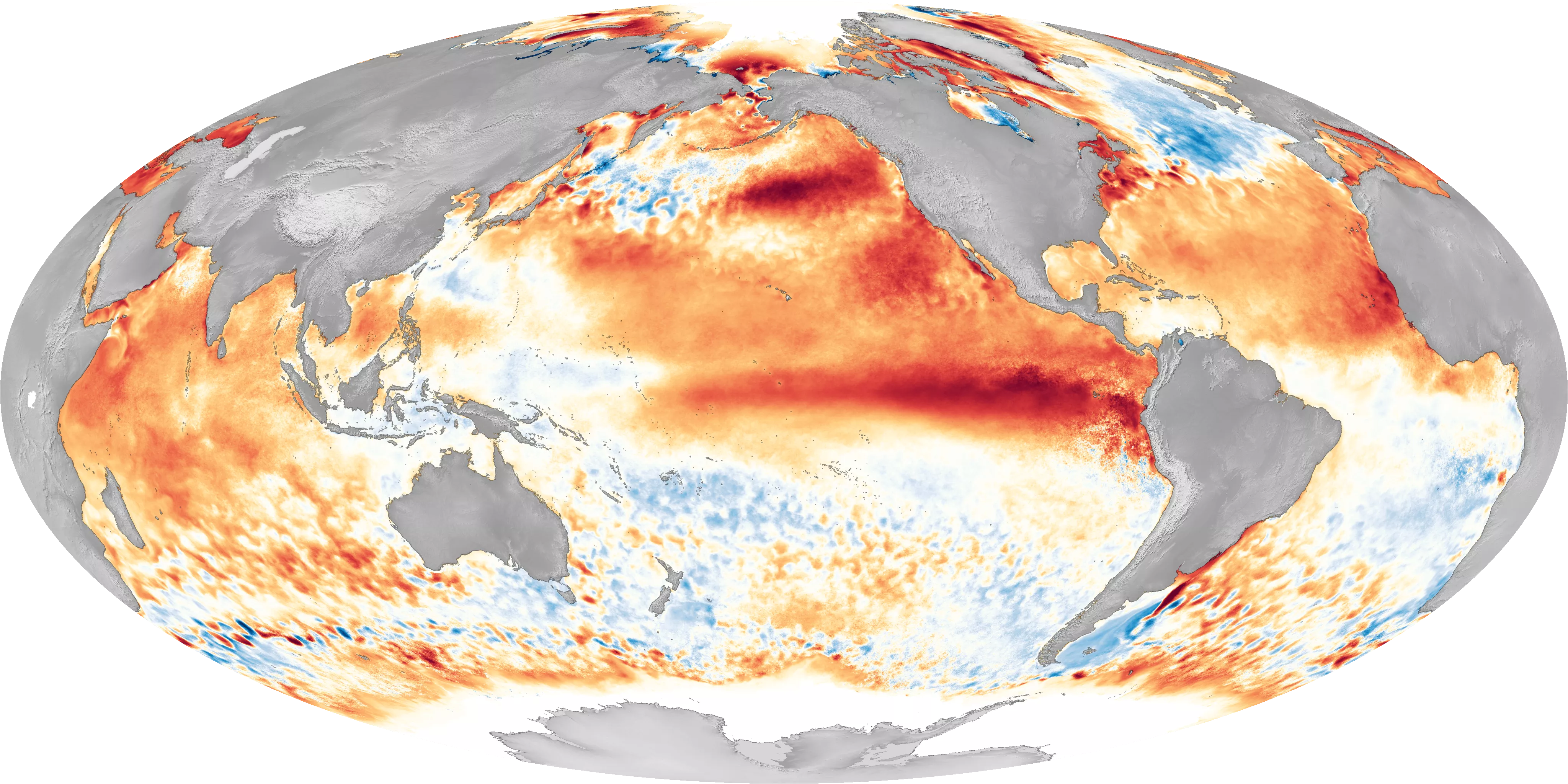

Source: NOAA/NESDIS

Source: NOAA/NESDIS

Summer and Hurricane Season

El Niño's summer influence is usually modest, but it still matters. While it can support periods of warmer conditions, particularly across parts of the northern and eastern U.S., it typically prevents those patterns from locking in. Instead of sustained heat, temperatures tend to cycle more frequently, limiting the duration of peak demand events.

That distinction matters for power markets. Summer heat can still be meaningful, and eastern load zones can still see hot stretches, but El Niño tends to break up the kind of long-duration, multi-region heat that creates broad, synchronized demand stress. The result is often a more regional and intermittent load profile rather than one large system-wide surge. In a Super El Niño year, however, the southern and southwestern U.S. can be an exception, where enhanced moisture and heat interactions can intensify localized extremes even as broader national heat risk is dampened.

The more important shift this year may be in the Atlantic hurricane season. El Niño typically increases upper-level winds across the basin, introducing wind shear that disrupts tropical development. The result is usually fewer and weaker storms, and in stronger El Niño setups, the basin can become meaningfully suppressed.

That has important implications for natural gas markets. Hurricanes have increasingly become a bearish shock mechanism, not because of supply loss, but because of demand and export disruption. Storms can knock out power demand through outages and business interruption, while also forcing LNG facilities to curtail operations or disrupting shipping flows. With U.S. production now overwhelmingly onshore, supply is far less vulnerable than in the past, so these events tend to leave more gas stranded domestically, weighing on prices.

A quieter hurricane season therefore removes one of the market’s key downside risks. Fewer storms mean fewer demand shocks and fewer LNG interruptions, allowing export flows and power demand to remain more stable through the summer. In that sense, El Niño-driven hurricane suppression skews bullish relative to baseline.

Winter Remains the Bigger Story

Winter is where El Niño tends to have the clearest and most consistent effect, and where a Super El Niño has the potential to move markets most materially. The jet stream often shifts farther south, which redirects the main storm track across the southern U.S. while reducing the frequency of Arctic air intrusions into the northern U.S. The result is typically warmer-than-normal conditions across northern regions and more active, wetter weather across the southern U.S.

For energy markets, that setup usually matters more than the summer signal. During El Niño winters, the jet stream often remains more active across the southern U.S., while the higher-latitude flow is less conducive to sustained southward releases of Arctic air from Canada. In other words, the pattern is less favorable for allowing dislodging polar vortex intrusions into the Lower 48 for extended stretches. That reduces the frequency and duration of Arctic outbreaks in major demand centers in the Midwest and Northeast, which are the main drivers of extreme heating demand and natural gas price spikes. In a Super El Niño year, this effect can become especially pronounced. The warmer bias across the northern tier can be both stronger in magnitude and more persistent through the season, leaving the winter demand profile substantially softer than it would otherwise be and meaningfully compressing the window for cold-driven price spikes.

Drought Could Still Complicate the Summer Outlook

One variable worth watching is persistent drought across parts of the South, especially Texas and the Southeast. Low soil moisture can amplify heat by limiting evaporative cooling, raising temperatures and increasing power demand. El Niño may help offset some of that risk by bringing more precipitation, but rainfall is often uneven and inconsistent, meaning broader drought conditions can still linger. A Super El Niño could bring heavier and more widespread precipitation to drought-affected areas, offering more meaningful relief, though the timing and distribution of that rainfall remains uncertain, and localized heat risk can persist even in wetter overall conditions.

If El Niño continues to strengthen toward a Super El Niño, the market implications become more pronounced. Summer risk may become less about persistent, synchronized heat and more about regional volatility, while hurricane activity may be sharply reduced by stronger wind shear, limiting one source of storm-related demand and LNG disruption. Winter, meanwhile, would likely be the more important signal, and the one where a Super El Niño could exert the most consequential influence. An extended mild pattern across key northern load centers would lower heating needs and substantially reduce the odds of extreme weather-driven demand.

About Stanwich Energy

Stanwich Energy is a trusted, independent energy advisory firm dedicated to helping organizations across the U.S. buy and manage energy more strategically. We provide energy procurement, sustainability solutions, risk management, reporting, and ongoing market intelligence supported by deep industry expertise and proprietary technology. Our client-first approach helps businesses reduce costs, optimize energy usage, and confidently navigate the complexities of today’s energy markets.

Ready to talk energy strategy? Share a few details on our Contact Us page and we’ll reach out to schedule a quick call.